Energy, Batteries and Data Centers: Monsson’s Integrated Model for Turning Energy Hubs into Digital Poles

The data center industry is going through a moment similar to that of renewable energy two decades ago: an accelerated technological wave, a significant need for capital, and a regulatory framework that must keep pace with investments. In this context, Monsson is betting on an integrated model – renewable energy, battery storage (BESS), and co-located data centers – to position Romania on the European map of critical infrastructure for AI and cloud.

In this interview, Sebastian Enache, Head of M&A at Monsson, explains the lessons learned from the development of the renewable market, the role of storage in supporting large energy consumers, and the company’s ambition to build a scalable data center platform of up to 200 MW across several strategic regions of the country.

As additional information, Sebastian Enache will also take the stage at DataCenter Forum 2026, where he will join a panel discussing the same parallel between the energy sector and the data center industry.

DataCenter Forum: In renewable energy, Romania has gone through stages of maturation and standardization. What lessons from the development of the renewable energy market do you believe could be applied to the local data center industry, especially in terms of permitting and grid integration?

Sebastian Enache, Head of M&A, Monsson: In renewable energy, Romania began shaping a strategic direction as early as 1999, and in 2003 the first large-capacity wind turbines for that time were installed. Although there were also discussions about photovoltaic parks, solar technology was not yet sufficiently advanced or competitive, so priority was given to wind power, which was the most efficient solution in that context. After nearly 25 years, we can see that both technologies have evolved significantly, are standardized, bankable, and almost equally widespread.

The main lesson is that every technological wave has critical, strategic moments when the regulatory framework, administrative capacity, and investors’ courage make the difference between stagnation and acceleration. In the early 2000s, everyone was talking about renewables, but few had real experience, the legislation was incomplete, and permitting processes were unclear. Only a handful of courageous investors chose to enter an immature sector, assuming significant risks.

Today, I see a clear parallel with the data center industry. If in renewables we are talking about large-scale equipment with a lifespan of 20–40 years that must generate energy in a stable and predictable manner, in the data center space we are discussing equally complex, long-term critical infrastructure that hosts technologies changing every two to three years. Servers can be replaced relatively quickly, but the energy, cooling, and connectivity infrastructure remains a long-term investment and requires legislative and operational predictability.

From the renewable sector’s experience, an essential lesson for data centers is the importance of a clear, coherent, and digitalized permitting process, as well as a transparent grid integration strategy. A lack of coordination between investors, grid operators, and authorities can delay critical projects for years. Conversely, forward planning of grid capacity and the designation of priority development zones can accelerate investments and reduce risks.

I believe there is a natural convergence between the two industries. Data center professionals need to collaborate actively with authorities, not only to highlight the importance of these investments but also to contribute to shaping a legislative framework adapted to technological realities. Fast construction, efficient grid connection, and location in suitable areas with robust energy infrastructure are critical elements if Romania is to capitalize on this new wave of development, just as it ultimately did in the renewable energy sector.

DCF: There is strong interest at Data Center Forum in sustainable investments. How do you see the role of energy storage (BESS) and renewable sources in supporting the operations of energy-intensive data centers – for example those dedicated to AI or cloud – in Romania and Europe?

Sebastian Enache

Sebastian Enache: The interest in sustainable investments in the data center sector is natural, especially given the accelerated growth in consumption driven by AI and cloud. From my perspective, battery energy storage systems (BESS) and renewable sources will play an essential role in supporting these operations in Romania and across Europe.

BESS technology is relatively new at large scale, but over the past five years it has experienced spectacular development, both technologically and economically. If in the past integrating a storage system was not financially feasible for most projects, today almost all modern wind and photovoltaic parks include BESS, and in parallel we are seeing the development of stand-alone systems dedicated to ancillary services. BESS is no longer just an add-on; it is an element that provides flexibility, stability, and predictability to the grid.

In this context, the parallel with data centers is evident. Until recently, BESS was not perceived as an essential component for a data center, where the focus was on traditional redundancy – diesel generators and UPS systems. However, as consumption grows and energy price volatility becomes a reality, storage systems will, in my view, become a standard component. Why? Because they enable cost optimization by purchasing energy at lower prices during surplus periods and using it during peak intervals. At the same time, they provide an additional layer of redundancy and can support the direct integration of local renewable generation.

Moreover, BESS facilitates the efficient connection of a data center to a green energy mix, reducing grid impact and increasing operational stability. For AI data centers, where power demand is high and constant, the combination of renewables, storage, and intelligent energy management can make the difference between a bankable project and one vulnerable to price and availability risks.

Monsson’s vision is clear: a data center is better positioned next to a renewable energy hub integrated with storage capacity than as an isolated consumer on the grid. By correlating the initial investment in generation and storage with the data center’s consumption profile, the overall project return can increase significantly – our estimates indicate a potential uplift of over 25%. In this way, sustainability is not just a branding objective, but a real competitive advantage.

DCF: Monsson is primarily known for its renewable energy and storage projects. What determined you to expand into data center infrastructure, and what synergies do you see between these two industries? (I’m thinking of the integrated model of energy + batteries + data centers.)

Sebastian Enache: I know Monsson is mainly recognized for developing renewable energy and storage projects, but expanding into data center infrastructure represents a natural evolution of our vision. As I mentioned earlier, our objective is to attract as much relevant energy consumption as possible in proximity to our production hubs. We believe the future belongs to the integrated model – energy + batteries + data centers.

In essence, the key is to bring consumption closer to production. In the traditional model, energy is generated in one area, transported over long distances, and consumed elsewhere, which involves losses, high grid-connection costs, and additional pressure on the network. By positioning data centers near wind and photovoltaic parks, integrated with BESS systems, we can optimize the entire investment chain. We reduce transport infrastructure costs, shorten implementation timelines, and create a far more efficient energy ecosystem.

For the data center developer, the advantage is strategic: access to competitive, predictable, and increasingly important green energy. For us, as a developer of renewable generation and storage capacity, integrating a large and constant consumer such as a data center increases the project’s financial stability and improves investment returns. Essentially, we are talking about an additional layer of optimization for all parties involved.

The synergies are also evident from a technical perspective. Batteries enable the balancing of renewable production and adaptation to the data center’s consumption profile. At the same time, the data center provides relatively stable demand, which supports the monetization of energy projects. In such a model, the national grid becomes a partner rather than the sole solution, and the pressure on public infrastructure is reduced.

We see this integrated model as a competitive advantage for Romania. As Europe searches for locations to develop AI and cloud capacity, the availability of large-scale green energy is a key criterion. If we can offer investors an integrated package – land, renewable energy, storage, and fast connection solutions – then we can transform energy hubs into digital poles.

For Monsson, this expansion does not mean stepping outside our area of expertise, but rather leveraging it in a more complex and efficient way. We believe the future of critical infrastructure is integrated, and the combination of energy, batteries, and data centers is a logical step in that direction.

DCF: Developing a 50 MW pilot data center in Romania is an ambitious undertaking. What are the main similarities and differences between investment dynamics in renewable energy and in data centers – from the perspective of regulation, financing, and scalability?

Sebastian Enache: Developing a 50 MW pilot data center is indeed an ambitious step, but from our perspective it is built on a solid foundation. We already have a 50 MW grid connection capacity through our hybrid project in Mireasa, where we operate 50 MW of wind, 35 MW of photovoltaic, and approximately 200 MWh of batteries. This combination provides ideal conditions to support a large-consumption data center safely and over the long term.

In terms of similarities, both renewable energy and data center investments are capital-intensive, depend on grid access, and require legislative and contractual predictability to be bankable. In both cases, investors look for regulatory stability, revenue visibility, and a clear development horizon.

The differences lie in technological dynamics and the regulatory framework. Renewable energy today benefits from a mature legislative environment, while for data centers there is not yet specific legislation or clearly defined zones where development is prioritized. This is why we aim to collaborate actively with authorities to help create a predictable and competitive framework.

We are engaging in this sector to support the development of the local data center industry and, just as we were pioneers in large-scale renewable energy projects, we aim to be among the first to build an integrated model in this industry as well.

DCF: Is the 50 MW pilot project just the beginning, or does it represent a replicable model? What plans do you have to transform this initiative into a broader expansion platform in the region?

Sebastian Enache: The 50 MW pilot project is not an isolated initiative, but the starting point of a replicable model that we intend to expand nationally and regionally. Our strategy targets the development of data centers with capacities between 50 MW and 200 MW in seven strategic areas of Romania, including Constanța, Satu Mare, and Arad. The selection of these locations is based both on access to robust energy infrastructure and on geographic positioning and connectivity to transport networks and fiber-optic infrastructure.

Our objective is to build an integrated platform in which renewable energy, battery storage, and large-scale consumption—represented by data centers—operate within an optimized ecosystem. The 50 MW model can be naturally scaled to 100 or 200 MW, following the same logic: local energy production, storage capacity, and infrastructure designed for phased expansion.

We aim to leverage Romania’s strategic geopolitical position. Although most data centers are currently concentrated in Western Europe, we see clear signals that Central and Eastern Europe, including Romania, can become a relevant hub for AI, cloud, and digital infrastructure. Through this platform, we intend to position Romania as a central point on Europe’s new digital map.

DCF: What are the biggest challenges you anticipate in integrating data centers with existing renewable energy and storage networks – from a technical, operational, or regulatory perspective?

Sebastian Enache: Challenges exist and will always exist when we talk about large-scale critical infrastructure. Integrating data centers with existing renewable energy and storage networks brings both opportunities and technical, operational, and regulatory challenges.

From a technical standpoint, the main challenge is grid capacity and managing energy flows in a stable and predictable manner. Data centers, especially those dedicated to AI or cloud, have high and constant consumption, and the grid must be able to support these loads without creating imbalances. However, a major advantage is that existing renewable projects are already connected to the grid and, in many cases, include BESS systems. This creates the conditions for co-locating data centers next to generation and storage capacity, reducing pressure on public infrastructure and offering a more efficient solution than in many other countries.

Operationally, the challenge lies in the intelligent integration of intermittent renewable production with the data center’s consumption profile. This is where batteries and advanced energy management systems come into play, ensuring flexibility, redundancy, and cost optimization.

From a regulatory perspective, permitting remains a critical point. At present, there is no dedicated framework that addresses in an integrated way the development of data centers in proximity to energy hubs. What is needed is clarity, predictability, and accelerated procedures for strategic projects.

As far as we are concerned, we bring part of the solution: grid connection capacity already available, mature technology, committed investments, and land prepared for development. The rest depends on collaboration with authorities and on investors’ appetite to capitalize on this opportunity.

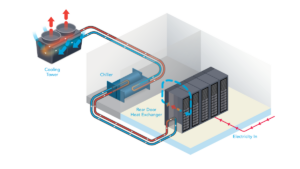

Liquid cooling is becoming the standard in AI data centers, with adoption rising from 14% in 2024 to 33% in 2025, and it is expected to reach 40% in 2026, according to Trendforce cited by Accenture. In the near future, data centers will use a combination of air-based and liquid-based cooling, while water-intensive evaporative methods will be phased out due to sustainability concerns and water scarcity.

Liquid cooling is becoming the standard in AI data centers, with adoption rising from 14% in 2024 to 33% in 2025, and it is expected to reach 40% in 2026, according to Trendforce cited by Accenture. In the near future, data centers will use a combination of air-based and liquid-based cooling, while water-intensive evaporative methods will be phased out due to sustainability concerns and water scarcity. Sustainability has become a central principle in data center design, influencing everything from prioritizing low-carbon materials and modular construction to water management, heat reuse, and integration of renewable energy.

Sustainability has become a central principle in data center design, influencing everything from prioritizing low-carbon materials and modular construction to water management, heat reuse, and integration of renewable energy.