Now in its seventh edition, the DataCenter Forum brought together approximately 700 participants and over 20 Romanian and international speakers on May 7, 2025, in Bucharest. Organized by Tema Energy – the local market leader in data center design and construction – the event highlighted the challenges and opportunities arising from the Artificial Intelligence revolution. From the explosion in computing power demand and energy consumption to massive investments in green energy driving energy stability, and Europe’s increased reliance on sovereign AI and cloud, speakers emphasized that we are at the beginning of a profound transformation that will shape the digital economy for decades to come.

Opening Keynote: The AI Revolution & Europe 4.0. Mihai Manole, Tema Energy: We Are Rapidly Reaching Unprecedented Levels of Computing Power and Energy Due to AI

Mihai Manole, Managing Partner of Tema Energy, opened this year’s edition with an overview of the AI revolution, comparing the industry’s dynamics between the US, Europe, and Romania. According to the CEO, while record-breaking global investments in AI infrastructure are being announced – $500 billion in the US, over €200 billion in the EU, more than $100 billion in China, and $50 billion in the UK – Romania currently has 59 data centers and data rooms, most of them small to medium-sized, with a vacancy rate of around 54%, similar to major European markets (FLAP).

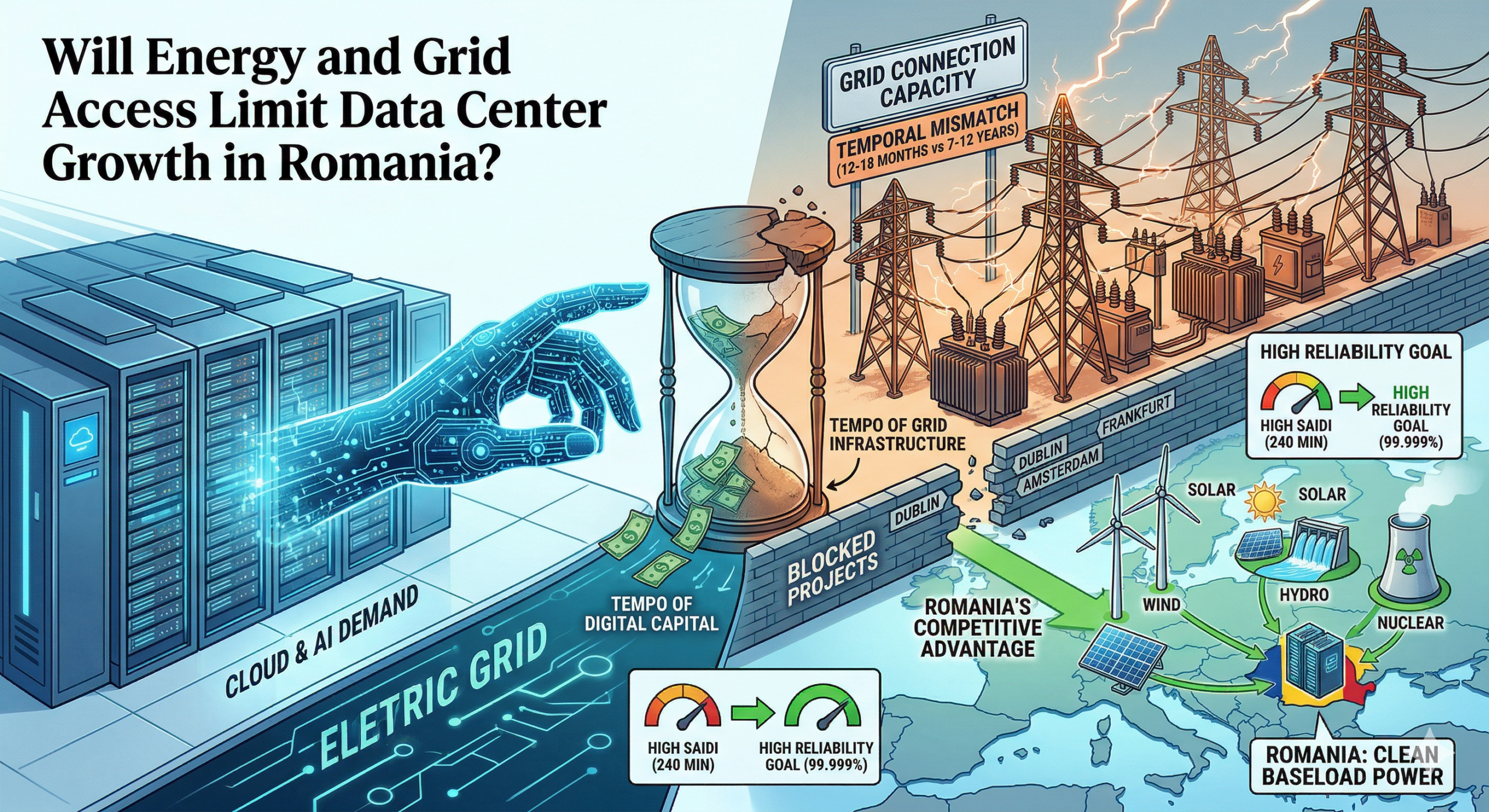

In terms of energy capacity, the US is building data centers totaling over 4,000 MW, China around 2,000 MW, and Europe surpasses 1,000 MW – compared to a global total of just 1,000 MW a few years ago. Romania, with 50% of its energy production from renewable sources and one of the most developed telecom networks in Southeastern Europe, has strong potential to attract significant international investments in this sector.

“Southeastern Europe has a relevant number of data centers, but installed power is low. On the other hand, we are at a very favorable moment for developing new data centers, and we are seeing very large green energy projects supported by the state or EU funds. Announced projects total 55 gigawatts from wind, solar, nuclear, and small modular reactors. These give Romania an advantage in energy stability and competitive pricing to attract international investor interest. What should Romania do to attract investments in this new data center and AI paradigm? First, authorities need to create a plan similar to what exists for attracting industrial and manufacturing companies. Because the new industry is IT and AI,” said Mihai Manole.

Keynote: Welcome to the AI Factory Era. Lessons Learned from Building the Largest AI Data Centers in the US – Wes Cummins, Applied Digital

The special guest of this edition was Wes Cummins – Founder and CEO of Applied Digital, one of the largest builders of AI data centers in the US, who successfully transitioned from crypto mining facilities to “AI factories.”

“To understand today’s level of tech adoption, consider this: ChatGPT, launched in November 2022, reached one million users in just five days. The fastest in any app’s history. Today, it has over 800 million users and around a billion queries per day. Google reached that daily query volume in 11 years. We’re talking two and a half years vs. 11. Also, if we look at the compute resources needed, Google uses 1,000 to 10,000 compute blocks per query, while ChatGPT uses between 300 billion and 1 trillion. These figures show the immense power required to run AI. This revolution will be built on data centers, much like the fiber-optic boom in the 1990s and early 2000s enabled the internet to become real,” said Wes Cummins.

According to him, the industry is facing unprecedented challenges in efficiency, capacity, and innovation not seen in the last 30 years.

“There will be many opportunities for innovative companies willing to take bold risks. During major industry shifts, as we are seeing now, is when new leaders emerge. We are at the start of a major transformation, perhaps one we may never witness again in our lifetimes,” he added.

Panel: Southeast Europe’s Data Center Market – Between Challenges and Opportunities

The event’s first panel featured Florin Popa (Orange Business Director, Orange Romania), Ion Paraschiva (Chief Commissioner, Head of IT Systems Management, Romanian Police), Alexandros Bechrakis (Digital Realty Hellas), and Radu Brașoveanu (PPC Romania).

Ion Paraschiva presented the Romanian Police’s perspective, mentioning the construction of a container-type data center (chosen for its relocatability), developed with Tema Energy. This helped bypass bureaucratic obstacles and accelerate operations for the more than 45,000 police officers currently active.

Florin Popa from Orange emphasized the rapid evolution of the local market in the past 12–18 months, marked by growing demand for colocation and infrastructure-as-a-service (IaaS, PaaS), along with increased interest in edge computing as companies seek proximity to customers. From Orange’s viewpoint, local challenges are not yet centered around AI, but around traditional use cases: B2B computing, back-up, and IT infrastructure. Data sovereignty compliance pressures are increasing, driving demand for local data centers.

“Energy consumption is rising, and the question is how fast it will rise and how we can support it – through transport and distribution networks and at the societal level. We’ll see how fast we can build these data centers and how we can support their massive compute needs. It’s critical to generate energy near data centers to avoid overloading the distribution grid. The key to all of this is digitalization,” added Radu Brașoveanu.

One of the panel’s conclusions, from Alexandros Bechrakis, was that regional markets are small and do not require massive investments, but rather well-directed ones.

“Romania, Greece, and other countries in our region are heading toward the third wave of development. In the next few years, we’ll see new centers built. Maybe not next year, but soon. At Digital Realty, we almost doubled our investment plan to nearly $8 billion, especially in US markets, but also in the FLAP region, as well as Greece, Romania, Spain, and Israel. We’re always seeking new markets, and all our European sites use 100% green energy,” he added.

Flash-chat: Trends Shaping the Data Centers of the Future – From Energy Efficiency to Edge Computing

The lineup of international speakers was rounded out by Mark Acton, one of the industry’s most prominent independent consultants. Acton has played a key role in shaping various industry standards and is a member of the European Commission committee responsible for the development of the EU Data Centre Code of Conduct – the main regulation for energy efficiency.

In the first Flash-chat of this year’s edition, Acton emphasized that data centers consume massive amounts of energy and that environmental responsibility is increasingly critical. According to him, Artificial Intelligence (AI) does not replace existing infrastructure—it augments it. As a result, the way we design data centers is changing.

“I wouldn’t call it a cold war, but it’s definitely an arms race,” said Acton. “Last week, Nvidia CEO Jensen Huang was asked whether China is lagging in AI, and he said no—in fact, they’re very close to the U.S. Clearly, we need to stay ahead and keep up with the pace of change. It’s a technological arms race, and I think the current geopolitical instability is prompting countries to focus more on their own regions. In Europe, I believe we’ll see more collaboration driven by these geopolitical shifts. Sovereign AI and sovereign cloud—our own technologies and data control—will become essential.”

Moreover, the focus is shifting from merely reducing the PUE (Power Usage Effectiveness) index to improving IT load efficiency—the real energy consumer in data centers. Acton also pointed out the need for greater public awareness. There’s a growing negative perception of data centers in the media, largely due to a lack of understanding of just how dependent society is on digital infrastructure. Users must become more aware of how their digital habits impact infrastructure and energy use.

Regarding regulation, Acton compared the data center industry to glassblowing—both require a lot of energy, and there’s often little clarity on how it’s used. Glassblowing took 15 years to be properly regulated; Europe is only just beginning the regulatory journey for data centers.

He also noted that established markets like FLAP-D (Frankfurt, London, Amsterdam, Paris, Dublin) are struggling to secure enough power, prompting a shift toward emerging markets. Romania has a real opportunity to join this map, with a favorable energy mix, high renewable potential, strong connectivity, and prospects for government support. Cities like Crete, Marseille, and Lisbon serve as inspirational examples.

Acton introduced the concept of “stranded energy”—excess energy generated by power plants that goes unused due to a lack of infrastructure for proper distribution. He warned that updating Europe’s energy grids could take up to 20 years. Meanwhile, SMR (Small Modular Reactors) technology could support future data center power needs, but public skepticism toward nuclear energy and a vague legal framework remain significant hurdles.

Panel – Ensuring Compliance in the Data Center Market: A Review of EU Regulations and Standards

Iolanda Saviuc (Scientific Officer at the Joint Research Centre, European Commission), Vanessa Moffat (representing the Data Centre Alliance), Nicola Hayes (CMO, Platform Markets Group), and Mark Acton discussed new EU regulations, including the EN50600 standard and Delegated Regulation (EU) 2024, which are still slow to adopt.

Panelists noted investors’ concerns over the complexity of new requirements but emphasized this as a moment of opportunity. By sharing data, engaging actively, and collaborating with European authorities, data center operators can shape future policies directly.

On the topic of incident reporting and the NIS 2 Directive, experts highlighted a major challenge: the data center industry has historically hidden security incidents. This lack of transparency undermines trust and the industry’s ability to learn and improve.

Saviuc and Moffat encouraged operators to get involved in EU stakeholder groups, challenge unrealistic proposals, and help ensure regulations reflect on-the-ground realities. Accurate data reporting is crucial to understanding the European data center landscape.

Acton stressed that the EU isn’t currently enforcing punitive measures—the goal is to introduce and promote best practices.

Flash-chat: Direct Liquid Cooling – The Future of Data Center Cooling

Philipp Guth, CTO of Rittal, spoke about how the German company is tackling the cooling challenges posed by AI. He highlighted two major trends transforming data center infrastructure: the explosion of large language models (LLMs) like ChatGPT and the rapid advances in chip manufacturing. New AI-optimized GPUs are incredibly powerful but also highly energy-intensive, with most of that energy converting directly into heat.

In this context, liquid cooling is no longer optional—it’s essential. Data centers need scalable, reliable cooling solutions capable of supporting AI workloads.

At the DataCenter Forum 2025 expo, Rittal showcased an innovative cooling system capable of delivering 1 MW of cooling capacity within the footprint of a standard rack. This solution is designed for both white and grey areas of data centers, with built-in scalability and redundancy—ideal for AI-ready infrastructures.

As demand for AI clusters grows, so does thermal density. Cooling systems must now offer both modularity and precision. Technologies like direct-to-chip cooling, which targets the heat source directly, provide superior thermal efficiency and reduce energy waste, Guth concluded.

Panel – The Tech Show Must Go On: Cutting-Edge Technologies Powering the Data Center Industry

This panel featured Flavia Chitanovici (Country Sales Manager, EnerSys Romania), Matteo Faccio (CTO, HiRef S.p.A.), George Dritsanos (Secure Power VP CEE, Schneider Electric), Igor Grdić (Regional Director Central Europe, Vertiv), Laurent Orvoën (Development and Innovation Sales Manager, Eneria), and Ramki Balasubramanian (International Sales – Technical, nVent).

Flavia Chitanovici outlined the main challenges facing critical infrastructure: pressure on power grids, the need for constant uptime, sustainability goals, and—above all—the skyrocketing energy demand driven by AI.

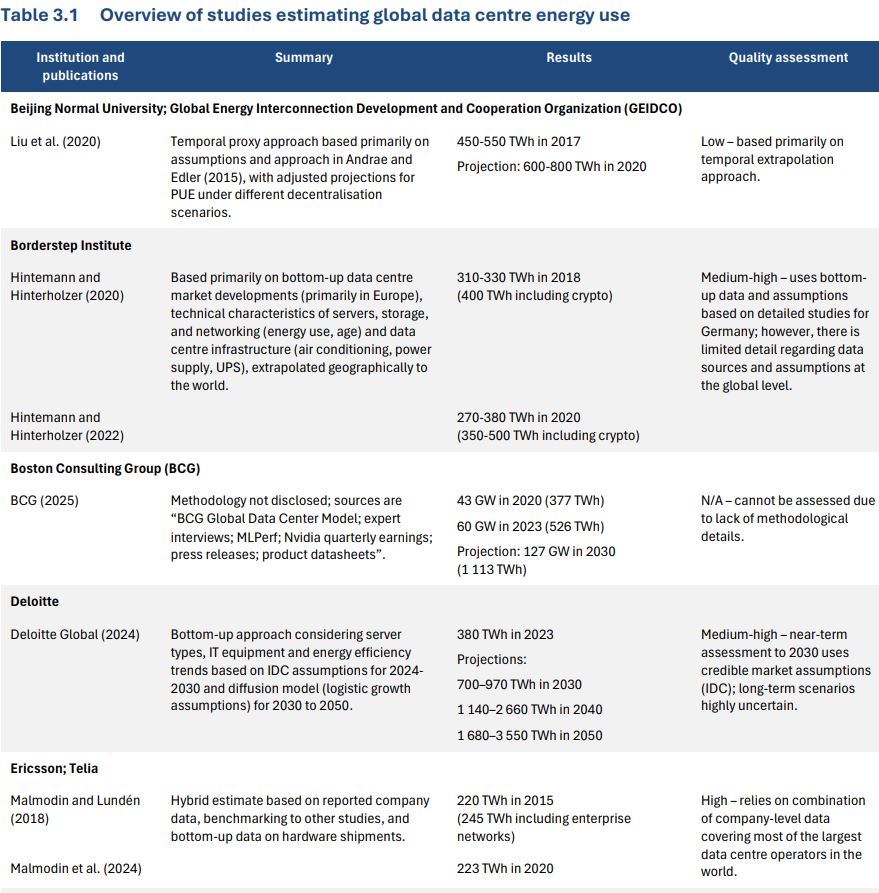

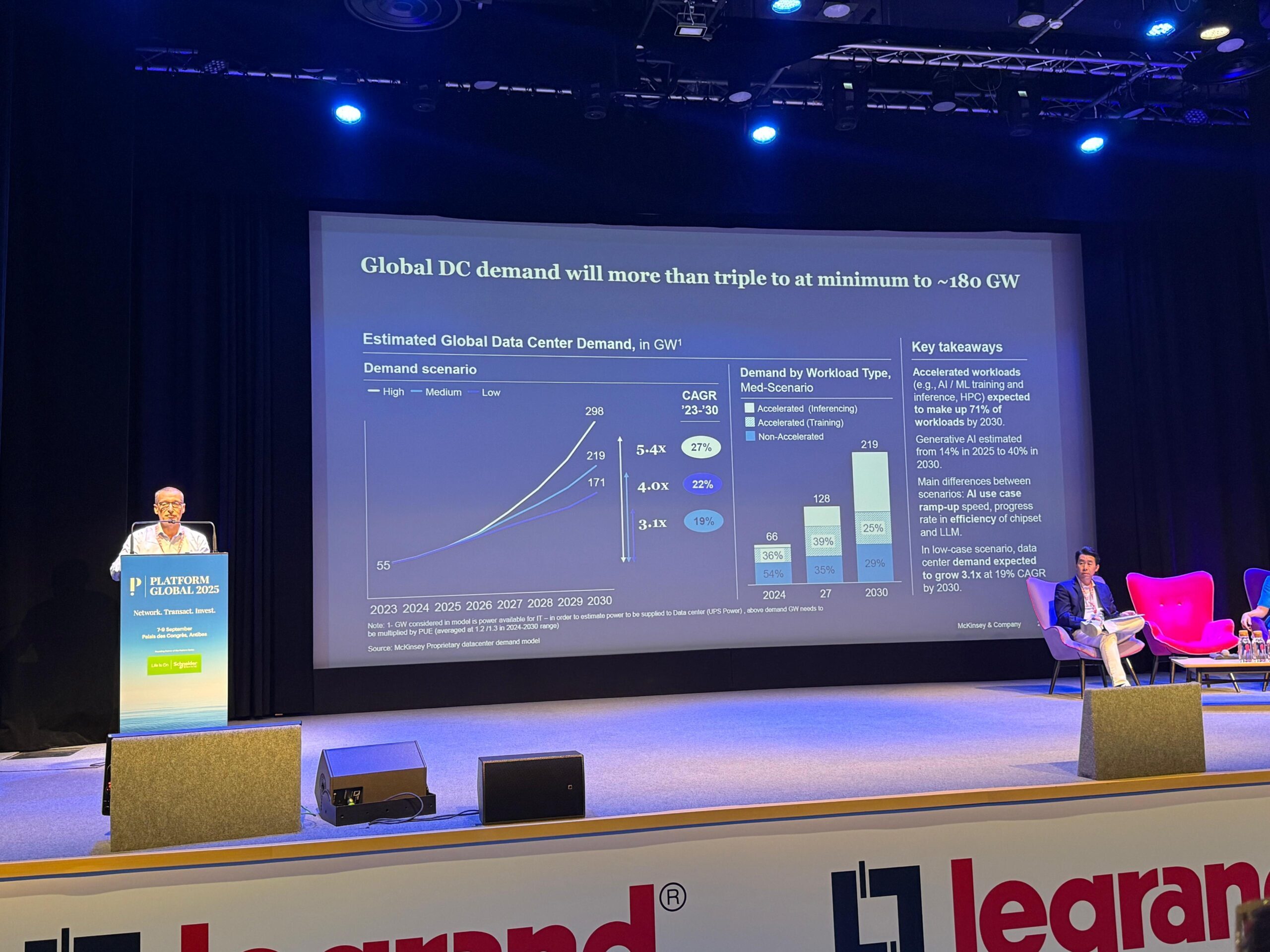

“Energy demand is growing so fast it’s outpacing infrastructure capacity. In 2024, data centers consumed around 415 TWh globally—1.5% of total global electricity use. And that number is growing up to 12% each year.”

This shift calls for a new paradigm: from simple back-up systems to intelligent energy management that supports long-term sustainability and resilience.

George Dritsanos discussed Schneider Electric’s commitment to sustainability, showcasing their microgrid-based approach and diverse portfolio of integrated solutions, including advanced software and solar energy storage. These solutions help data centers become more energy-efficient, sustainable, and future-ready.

Igor Grdić shared Vertiv’s perspective, highlighting how AI factories and GPU-driven centers, especially those with Blackwell series GPUs, present a unique challenge. Unlike the steady-state nature of traditional cloud workloads, AI servers generate sharp fluctuations in power usage—varying by up to 20 MW within milliseconds in a 100 MW site. Vertiv’s systems are built to handle such volatility.

Flash-chat: Vodafone Managed Services for Data Storage and Management

Dinu Dragomir, Director of Vodafone Business Romania, highlighted the company’s commitment to supporting businesses of all sizes and public institutions. Since 2024, Vodafone has offered its own public cloud (VPS) and private cloud (Virtual Data Center), hosted in Vodafone-operated data centers. He also noted the completion of Romania’s first government cloud and discussed the company’s internship program, which helps young people start and grow their careers at Vodafone.

Panel – The Role of AI in Technology: How Artificial Intelligence is Changing the Way We Work and Live

Speakers included Gabriel Pavel (Regional Director, Fsas Technologies), Mihai Logofătu (Co-founder & CEO, Bittnet Group), Tudor Cosăceanu (Regional VP, UiPath), and Bogdan Tudor (Founder, StarTech Team and CEO, Class IT Group).

Gabriel Pavel announced that Fsas Technologies will launch an energy-efficient AI processor in 2026 aimed at helping the entire industry.

Bogdan Tudor revealed that, for the past eight years, his organization has solved about 80% of user support requests and 90% of tech incidents using AI-powered software bots that diagnose and solve issues autonomously.

Mihai Logofătu explained how Bittnet integrates AI across internal processes, from employee relations to investor communications. “The impact is real. This is an irreversible transformation that must be viewed in its entirety,” he said.

Tudor Cosăceanu demonstrated UiPath solutions like “Document Understanding,” which uses AI to read and interpret documents, including doctors’ handwritten notes.

Inspiration Moment with Virgil Stănescu

Virgil Stănescu—former national basketball team captain and five-time MVP of Romania—shared insights on how we measure success and performance in both sports and technology. He recounted a moment from a podcast with chess legend Garry Kasparov, who said, “Work is talent.” According to Stănescu, we train and work 90% of the time to perform 10% of the time—and passion for that 10% is what makes the difference.

Awards Ceremony – DataCenter Forum 2025

The event closed with awards recognizing the most notable contributions in Romania’s data center industry:

- Cloud Services Provider of the Year: Vodafone Romania – accepted by Dinu Dragomir

- Hyperscale Regional Development of the Year: Digital Realty – accepted by Alexandros Bechrakis

- Digitalization of the Year – Public Institutions: General Directorate for Internal Protection, MAI – accepted by Florin Vizireanu

- AI Infrastructure Solutions for Data Centers: Rittal – accepted by Marius Totolici

- Press Contribution of the Year: Ziarul Financiar – accepted by Cristian Hostiuc

Conclusion

DataCenter Forum 2025 spotlighted the fast-paced transformation of the data center industry, driven by the AI revolution, rising power demands, and sustainability pressures. The surge in GPU clusters and the emergence of AI factories bring new challenges in cooling, energy consumption, and infrastructure stability. The industry is responding with tangible solutions: direct-to-chip liquid cooling, high-density modular systems, microgrids, and AI-powered operations. These technologies are reshaping data centers into smarter, more efficient, and more sustainable ecosystems—with a growing impact on both public and private digital transformation.